Ohio Electrician Insurance

9:00am - 5:00pm Mon-Fri

We'll Reply in 15min*

A single lawsuit from a damaged panel or a house fire traced back to faulty wiring can cost an electrical contractor tens of thousands of dollars, sometimes more. Ohio's regulatory framework adds its own requirements on top of that risk, including bonding, licensing, and mandatory workers' compensation for most employers. Whether you're a solo electrician pulling permits in Columbus or running a 15-person crew across Cincinnati and Cleveland, understanding your insurance obligations isn't optional. It's the difference between building a sustainable business and watching one bad job wipe out years of profit. This guide breaks down the cost and coverage details specific to

Ohio electrician insurance, from baseline requirements to smart strategies for keeping premiums manageable without exposing yourself to unnecessary risk.

Core Insurance Requirements for Ohio Electricians

Ohio doesn't treat electrical work casually. The state maintains specific licensing, bonding, and insurance requirements that every contractor must meet before pulling a single permit. Failing to comply can result in fines, license suspension, or personal liability for damages that would otherwise be covered.

State Licensing and OCILB Bond Requirements

The Ohio Construction Industry Licensing Board (OCILB) oversees electrical contractor licensing statewide. To obtain and maintain your license, you'll need to pass an examination, show proof of experience, and post a surety bond. The bond amount varies, but most electrical contractors are required to carry a bond ranging from $5,000 to $25,000 depending on the type of license and scope of work.

A surety bond isn't insurance for you. It protects the public and the state if you fail to meet contractual or legal obligations. If a claim is paid against your bond, you're responsible for reimbursing the surety company. Many new contractors confuse bonding with liability coverage, which is a costly mistake. You need both, and they serve entirely different purposes.

Some municipalities, including Columbus and Cleveland, impose additional local licensing requirements on top of OCILB standards. Check your local electrical licensing requirements before bidding on work in a new jurisdiction.

General Liability: The Foundation of Your Policy

General liability insurance is the policy most Ohio electricians purchase first, and for good reason. It covers third-party bodily injury, property damage, and personal injury claims that arise from your work. If a homeowner trips over your extension cord and breaks a wrist, or if your installation causes water damage to a client's ceiling, general liability responds.

Ohio electrical contractors typically pay between $90 and $300 per month for general liability, which runs approximately 10% below the national average. Most policies carry limits of $1 million per occurrence and $2 million aggregate, though commercial clients and general contractors often require higher limits before allowing you on a job site.

One common gap we see: general liability doesn't cover your own injuries, your employees' injuries, or damage to your own tools and equipment. Those require separate policies.

Workers' Compensation in the Buckeye State

Ohio operates a monopolistic state fund for workers' compensation through the Bureau of Workers' Compensation (BWC). Unlike most states where you shop among private insurers, Ohio requires employers to purchase coverage directly from the BWC or qualify as a self-insured employer. Sole proprietors without employees can opt out, but doing so means you have zero coverage if you're injured on the job.

Rates are calculated based on your payroll, your industry classification code, and your claims history. Electrical work carries a higher risk classification than many trades, so expect your per-$100-of-payroll rate to reflect that. The BWC publishes its

rate schedules and fee structures annually, and participating in safety programs or group rating plans can reduce your premiums significantly.

By: Aaron McElwain

President of Bellwether Insurance

Beyond the basics, several optional policies fill gaps that general liability and workers' comp leave exposed. The right combination depends on your business size, the type of work you perform, and how much equipment you own.

Commercial Auto and Fleet Insurance

If you use vehicles for business purposes, your personal auto policy won't cover accidents that occur during work. Commercial auto insurance covers liability and physical damage for trucks, vans, and service vehicles used to travel between job sites. Ohio commercial auto premiums for contractors vary based on fleet size, driver records, and vehicle types, but most solo electricians can expect to pay $150 to $250 per month for a single vehicle.

Don't overlook hired and non-owned auto coverage if your employees occasionally drive their personal vehicles for work errands. A gap here can leave you liable for accidents your employee causes while picking up supplies in their own car.

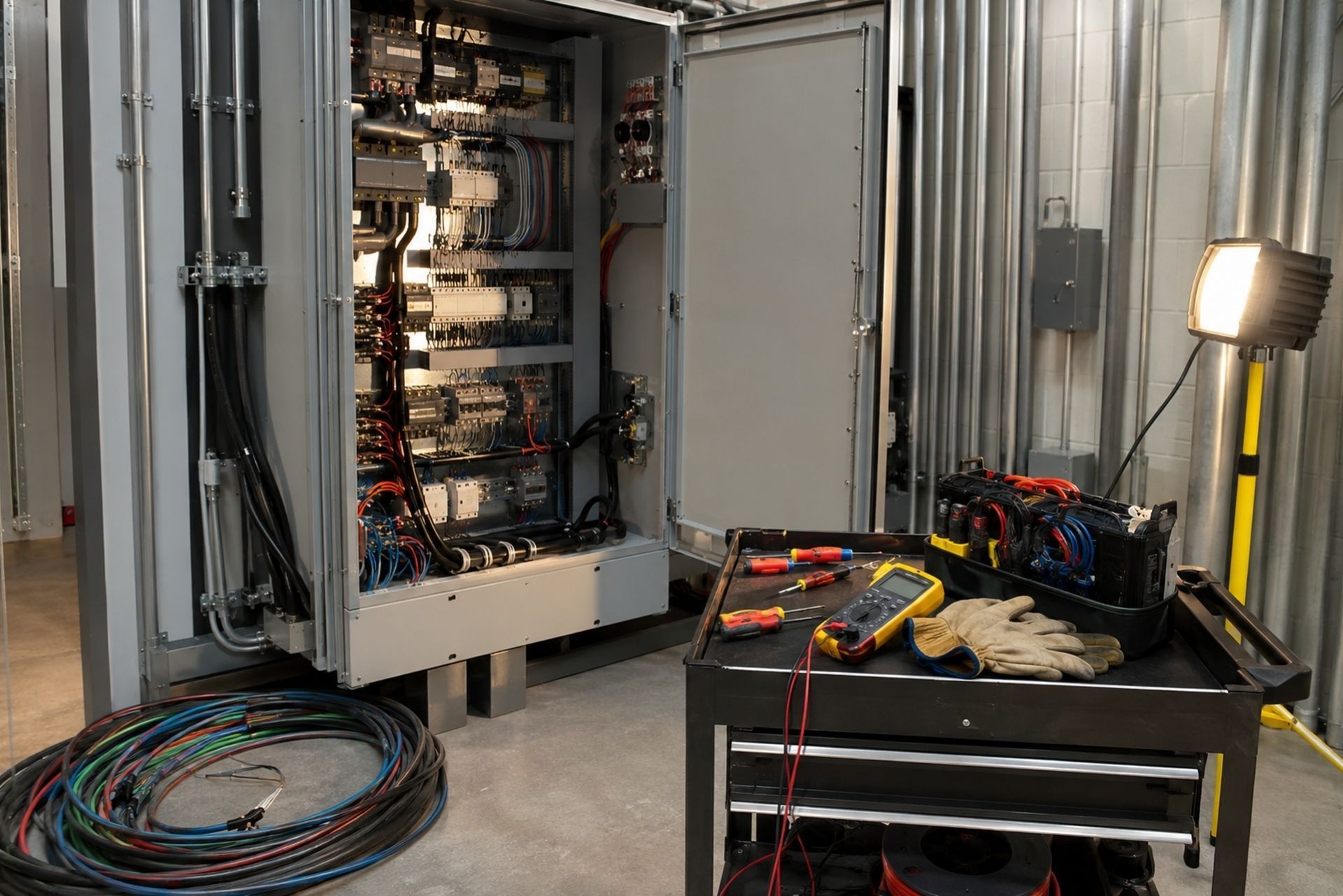

Inland Marine: Protecting Tools and Equipment

Your oscilloscope, wire pullers, conduit benders, and diagnostic equipment aren't cheap. Standard commercial property policies often exclude tools in transit or at job sites. Inland marine insurance fills that gap, covering your tools, equipment, and materials wherever they go.

Premiums for inland marine are relatively low compared to the replacement cost of a fully stocked service van. Most electricians pay $30 to $75 per month depending on the total value insured. Given that a single theft from an unlocked van can cost $5,000 to $15,000 in tools alone, this coverage pays for itself quickly.

Professional Liability vs. General Liability

These two policies cover different types of claims, and confusing them is a frequent mistake among contractors.

| Feature | General Liability | Professional Liability |

|---|---|---|

| Covers | Bodily injury, property damage | Errors, omissions, faulty design |

| Example Claim | Client slips on debris at job site | Incorrect load calculation causes panel failure |

| Required By | Most clients and GCs | Some commercial contracts |

| Typical Monthly Cost | $90 - $300 | $50 - $150 |

| Also Called | CGL or GL | E&O Insurance |

If you perform any design work, energy audits, or consulting alongside your installation services, professional liability becomes essential. A general liability policy won't cover a claim alleging your design recommendation caused a system failure six months after installation.

Comparing Coverage Needs: Residential vs. Commercial

The scope of your work shapes your insurance needs more than most electricians realize. Residential electricians typically face lower liability limits, simpler contracts, and fewer coverage requirements from clients. A homeowner hiring you to rewire a kitchen rarely asks for a certificate of insurance.

Commercial and industrial work is a different situation entirely. General contractors on commercial projects routinely require $1 million/$2 million GL limits, and some specify $5 million umbrella policies. You may also need to list the GC and property owner as additional insureds on your policy, which your insurer can endorse for a small fee.

The claims profile differs too. Residential work generates more slip-and-fall and minor property damage claims. Commercial work tends to produce larger, less frequent claims, often involving code violations, project delays, or equipment damage. Your insurer will price your policy accordingly based on the percentage of revenue derived from each sector.

Average Cost of Ohio Electrician Insurance

Understanding what you'll actually pay helps you budget accurately and avoid sticker shock. Ohio's insurance costs for electricians fall below the national average for general liability, but total annual spend depends on how many policies you bundle.

Factors That Influence Your Monthly Premiums

Your premiums aren't arbitrary. Insurers weigh several variables:

- Annual revenue and payroll: higher numbers mean higher premiums

- Years in business: newer contractors pay more due to lack of claims history

- Claims history: even one prior claim can increase rates by 10% to 30%

- Type of work: commercial and industrial carry higher rates than residential

- Number of employees: more workers mean more exposure

- Subcontractor use: hiring uninsured subs can increase your liability

A solo residential electrician with $150,000 in annual revenue and no claims history might pay $1,200 to $2,000 per year for general liability alone. A commercial contractor with five employees and $750,000 in revenue could pay $4,000 to $8,000 annually for a similar policy. These figures shift based on your specific risk profile, and getting accurate quotes requires providing detailed business information to your agent.

Ways to Lower Insurance Costs Without Losing Coverage

You don't have to accept the first quote you receive. Several strategies can reduce your premiums without stripping away necessary protection:

- Bundle policies into a Business Owner's Policy (BOP) for multi-policy discounts

- Maintain a clean claims history by investing in safety training

- Join a BWC group rating program for workers' comp savings of 20% to 50%

- Increase your deductible if you have cash reserves to cover smaller claims

- Review your policy annually to remove coverage you no longer need

- Work with an independent agent who can compare multiple carriers

One overlooked tactic: document your safety protocols and training records. Insurers reward contractors who can demonstrate a proactive approach to risk management.

Common Questions About Ohio Electrical Insurance

Do I need insurance if I'm a sole proprietor with no employees? General liability is strongly recommended even without employees. Many clients and permit offices require proof of coverage. Workers' comp is optional for sole proprietors in Ohio, but you'll have no injury protection without it.

Does my insurance cover subcontractors I hire? Generally, no. Your policy covers your employees and your business operations. Uninsured subcontractors can create liability exposure for you, so always verify their coverage and get certificates before they start work.

How quickly can I get a certificate of insurance? Most insurers issue certificates within 24 to 48 hours of binding a policy. Some digital-first carriers provide same-day certificates. If a GC needs proof before you start a job Monday morning, plan accordingly.

What happens if I let my insurance lapse? Ohio's contractor insurance requirements tie coverage to licensing in many jurisdictions. A lapse can trigger license suspension, and any claims during the gap period become your personal financial responsibility.

Is a surety bond the same as insurance? No. A bond guarantees your performance to the public. If a bond claim is paid, you owe the surety company back. Insurance pays claims on your behalf without requiring reimbursement, within your policy limits.

The Bottom Line: Protecting Your Trade

Running an electrical contracting business in Ohio means managing real financial risk every time you open a panel or pull wire through conduit. The right insurance package protects your livelihood, satisfies state and local requirements, and gives clients confidence in hiring you.

Start with general liability and workers' compensation as your foundation. Add commercial auto if you drive to job sites, inland marine if your tools leave your shop, and professional liability if you do any design or consulting work. Review your coverage annually as your revenue, headcount, and project types evolve.

The cost of adequate Ohio electrician insurance is predictable and manageable. The cost of being uninsured or underinsured is neither. Get quotes from at least three sources, work with an agent who understands contractor risks, and treat your insurance spend as a non-negotiable business expense, not an afterthought.

About The Author:

Aaron McElwain, CIC

As President of Bellwether Insurance, I’m passionate about helping individuals and businesses protect what matters most through honest advice and reliable coverage. With my Certified Insurance Counselor (CIC) designation and years of industry experience, I focus on simplifying insurance, building lasting relationships, and delivering peace of mind through every policy we write.

OUR PERSONAL INSURANCE COVERAGE IN OHIO

Explore Personal Insurance Coverage in Ohio

We only work with outstanding insurance companies that offer great value and continually impress our clients.

Home Insurance

Protecting Ohio homes, ensuring comfort

Life Insurance

Safeguard futures, cherish moments

Umbrella Insurance

Extra coverage, ultimate peace

Car Insurance

On the road, confidently insured

Condo & Renters Insurance

Customized policies, worry-free living

Motorcycle Insurance

Ride fearlessly, enjoy the journey

Choose Bellwether Insurance Today for Personalized Protection

Get a Plan Tailored to Your Lifestyle

Bellwether Insurance evaluates the risks you and your family face, taking into account your assets, personal circumstances, and individual requirements to create a tailored insurance solution.

Recover with Confidence

With our personal insurance coverage, you'll be prepared to bounce back from unforeseen events that could have left you and your family in a difficult financial situation.

Avoid Overpaying

Through customized insurance plans, you'll receive adequate coverage without unnecessary costs. At Bellwether Insurance, we strive to keep premiums cost-effective while providing the protection you need.

Review from our Clients

Customer Testimonials

See why Ohio residents work with Bellwether Insurance Agency in LaGrange, Ohio

Arun K.

Personal Insurance Client

After a decade old relationship with a premium and commercial insurance provider.. my switch to Bellwether has left me wondering why I waited so long. Primarily my experience has been dealing with Jessica Fox.. and she's been awesome to work with. She's super responsive, stays on top to follow up on your enquiries and really gets things done to delight customers.

Rob J.

Personal Insurance Client

Absolute pleasure to work with. Sandra has taken care of all my insurance needs for over 2 years now. Bellwether was able to save me quite a bit of money over previous carrier. Always giving heads up on any changes, or weather it’s time to check for new price she’s on top of it. I recommend them often to friends and family.

Nick W.

Personal Insurance Client

Aaron and Sandra are amazing! I faithfully stayed with my previous insurance for over ten years until I had them review my policies. Wish I would have done it years ago. Saved me quite a bit of money as well as gaining coverage what's not to love? They respond very quickly and professionally. I work in sales as a profession so it's great to see that level of attention and attentiveness provided here. Stop your search and give them a shot you won't regret it. On a side note even though it is something so small I love the fact they send laminated copies of insurance cards anytime you make a change. 10/10

Bobby P.

Personal Insurance Client

Bellwether Insurance is the best ever! Always there when I need them and always has the answers with quick replies. I will never go with a different Insurance Agent. If I could, I would give then a 10 Star review! Thanks Sandra for all your help!